Daily SITREP for Friday, March 17, 2023

Welcome to the SITREP for Friday, March 17, 2023.

Two very different banking crises played out this last week and, while both seem to be over, the panicky reactions in world markets indicates a lot of FUD (fear, uncertainty, and doubt) has built up. This suggests that companies won’t get the benefit of the doubt if there’s a stumble or any sign of weakness.

In the case of SVB and Credit Suisse, there are some important takeaways with respect to risk management and communications which I’ll sum up in Tuesday’s email.

There’s a new government in Tunis but its appointment is contentious and comes against the backdrop of increasingly rough treatment of migrants from sub-Saharan Africa, all of which is raising the tension in Tunisia. There’s good news farther east, however. First, as the peace deal between Ethiopia and the Tigray region seems to be holding and second, as China’s efforts to become a peacemaker seem to have pushed Saudi Arabia and Iran towards rekindling an old peace deal.

On the economic front, despite China’s increased economic activity, oil and shipping are both down significantly, with analysts suggesting that we’re not at the bottom yet for either. And finally, it seems that the Russian downing of a US drone over the Black Sea wasn’t accidental: a reminder of the ‘strategic corporal’ concept where the actions of a relatively junior soldier can have significant effects when stakes are high.

If this is your first time receiving this email, greetings! These SITREPS (situation reports) contain updates on critical events and essential metrics for you to use in your decision-making. There’s a guide here and a detailed white paper about the small data approach to risk assessment here.

Let’s go.

Rough Times for Banks

The run on Silicon Valley Bank (SVB) last weekend is now under control with the US FDIC administering the bank and guaranteeing access to deposits for SVB’s customers. This averted the knock-on effects many had feared if the companies who relied on SVB ran out of money, which would have hit not just Silicon Valley, but the businesses and firms that relied on these tech companies to run their firms. (There are good summaries of these second-order effects in Bloomberg and the FT.)

However, SVB’s rapid collapse made many observers jittery and unwilling to give other banks the benefit of the doubt, particularly after Signature Bank’s collapse a few days earlier. These fears threatened First Republic Bank which needed $30bn from larger institutions to stay afloat, while mid-sized banks saw an incredible outflow of cash over the last week as customers moved their money to the larger institutions. (See the FT for more.)

There are also suggestions that mid-sized US banks will face increased controls to avoid under capitalization, which might push some other banks out of business if they’re unable, or unwilling, to meet additional regulations. (See Reuters for more.)

Meanwhile, Swiss bank Credit Suisse, had a rough week after its requests for additional support were rejected by the Saudi National Bank, requiring the Swiss Central Bank to provide $45bn in credit to keep the bank afloat. The problems at Credit Suisse are unrelated to SVB and the bank has been weak for some time but this played (plays?) into the narrative of a global bank run. The worst seems to be over in the US but Credit Suisse appears to have systemic weaknesses – like its atrocious risk management I wrote about on March 3rd – that even a cash injection won’t solve. (The FT has a long article on Credit Suisse here.)

President Xi as Middle East Peace Broker?

Saudi Arabia and Iran announced that they were reopening diplomatic ties, which had been broken for over seven years. This announcement caught many by surprise but appears to have been largely due to diplomatic efforts by China. (See the NYT for more.)

This is a positive development for regional security and a win for Iran, but the absence of any US involvement in the deal strengthens the perception amongst many that the US is no longer engaged in the region.

However, rather than a lack of US support to the region, this is more suggestive of China’s growing interest in engaging in global diplomacy, something that Beijing had shunned for many years. This is also a sign that Riyadh, under Crown Prince Mohammed bin Salman, is keen to build partnerships with countries like China that support his ambitious construction and expansion plans. (See Bloomberg for more.)

Two Global Friction Points

A Russian jet caused a US drone to ditch in the Black Sea earlier this week. Initially, this was described as an accident by Moscow but video from the drone appears to show the jet ‘buzzing’ the drone before dumping fuel in its path, causing it to crash. (See Reuters for more.) On one hand, this is a small action but when tensions are high, and an active conflict zone is so close, small actions like this have the potential to spiral, a concept sometimes referred to as the strategic corporal.

A Russian Su-27 military aircraft dumps fuel while flying by a U.S. Air Force MQ-9 “Reaper” drone over the Black Sea, March 14, 2023 in this still image taken from handout video released by the Pentagon via REUTERS

Meanwhile, tensions around the South China Sea and Taiwan are also high and both the US and Chinese navies are very active in these areas. In some places, the navigable waterways are relatively narrow, putting vessels into close proximity, again increasing the possibility that a thoughtless action, or accident, could quickly spiral. (More on Reuters.)

Is There an Oil and Container Glut?

Both oil and container prices are at low points due to oversupply with shipping having dropped over 25% in the last few weeks alone.

Analysts believe that even with China’s increased demand, oil supplies remain robust as Russia’s production remains high. This oversupply has pushed oil to a 15-month low but prices may remain volatile for some time as a range of factors is affecting the price. (See Bloomberg for more.)

Container shipping is at levels not seen since before the pandemic with the FBX container index down around the $1,500 mark, a $500 drop from only a couple of weeks ago.

2023 Freight Rates from our friends at Freightos

This suggests an oversupply of shipping inventory that’s not yet matched by demand, suggesting that shipping will remain cheap for some time.

Xeneta CEO Patrik Berglund said in late November that if spot rates had not stabilized and started to rise again by the first and second quarters of this year, “carriers have played this market really badly.”

By that definition, ocean carriers have played this market really badly.

Analyst Greg Miller in Freightwaves

Nevertheless, China’s economy seems to be back on track so these low prices may not last. (See Bloomberg for more.)

On to the numbers.

Key Metrics

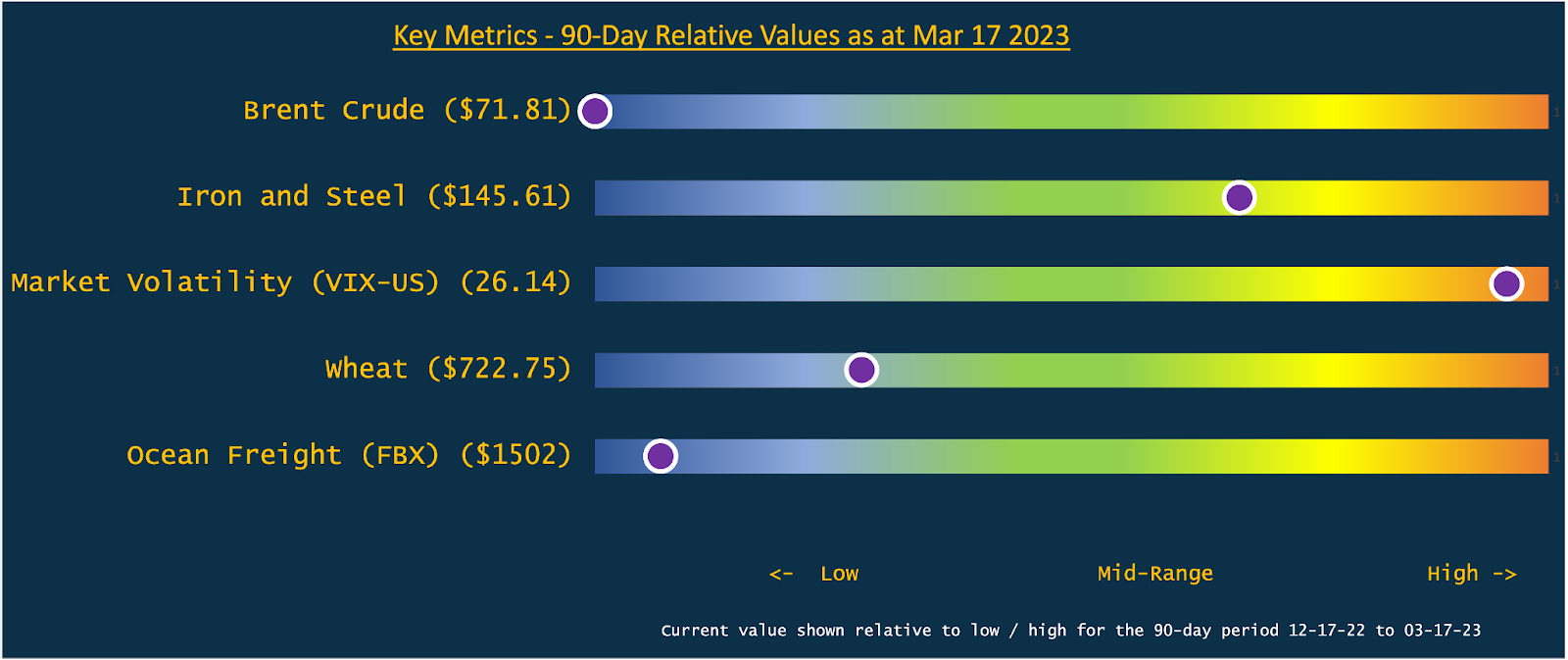

90-Day Relative Values

↻ Turn your phone for a better view

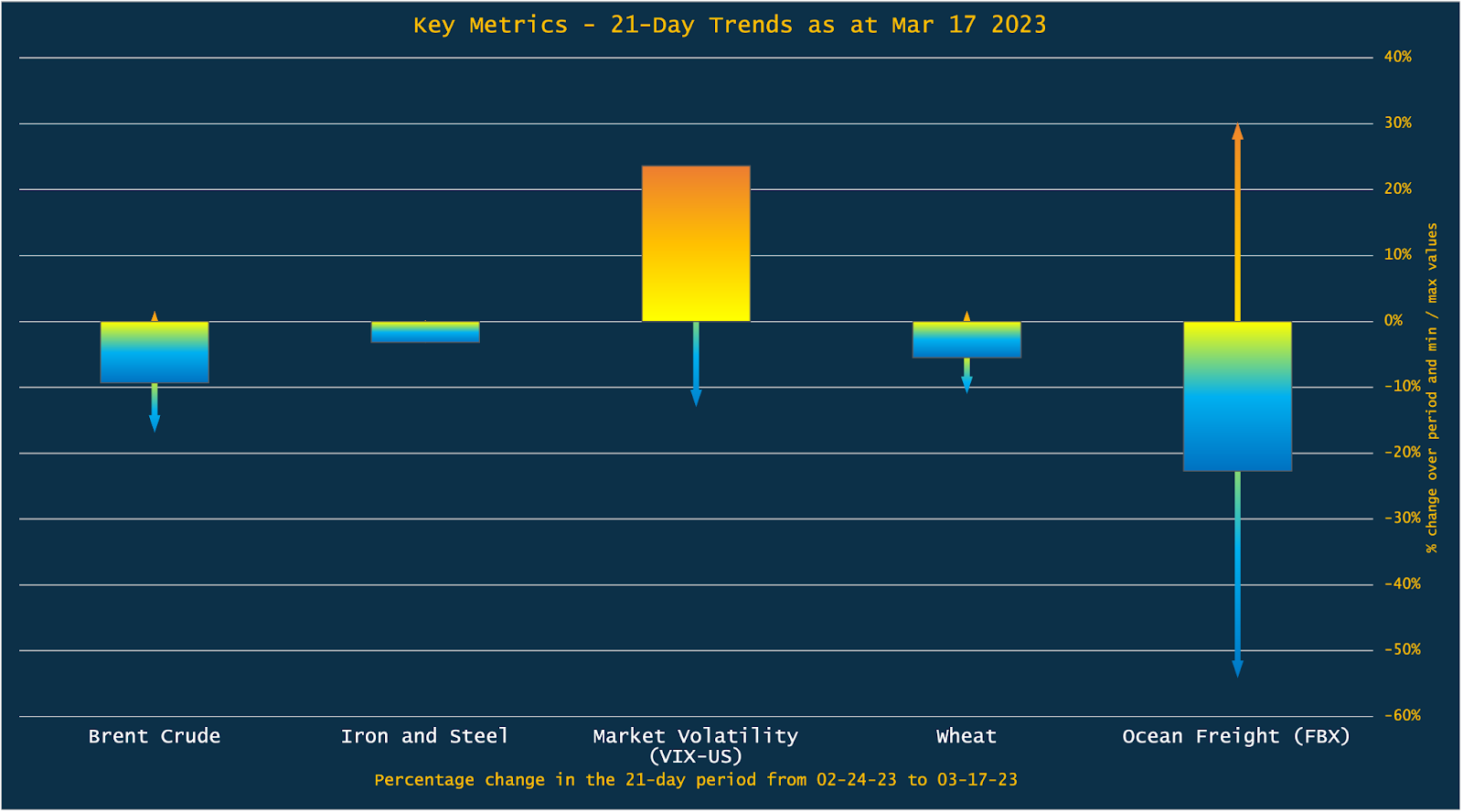

21-Day Trends

↻ Turn your phone for a better view

Oil (Brent Crude)

Brent Crude is very low for this 90-day interval. Prices decreased moderately over the last 21 days after significant fluctuation.

Iron and Steel

Iron and Steel are high for this 90-day interval. Prices decreased moderately over the last 21 days after slight fluctuation.

Market Volatility

Market Volatility (VIX) is very high for this 90-day interval. The index increased sharply over the last 21 days after moderate fluctuation.

Wheat

Wheat is low for this 90-day interval. Prices decreased moderately over the last 21 days after significant fluctuation.

Shipping (FBX)

Shipping (FBX) is very low for this 90-day interval. Prices decreased sharply over the last 21 days after significant fluctuation.

Election Watch

- 2 April: Finland, Parliament

- 30 April: Paraguay, President, Senate and Chamber of Deputies

Palate Cleansers

We’re all just one file deletion away from armageddon…

That’s it for today. Have a great weekend and I’ll see you on Tuesday with some takeaways for risk and communications managers that we can learn from SVB and Credit Suisse.

All my best

Andrew

Disclaimer

These SITREPS are provided for informational and educational purposes only. Comments or observations are my own and do not reflect the opinions of any firms I am associated with. The sources from which the metrics are derived are obtained from sources believed to be accurate and reliable, however due to the possibility of human and mechanical error or other factors, Andrew Sheves / Tarjuman LLC is not responsible for any errors or omissions.